In its June report “2021 Trends and Emerging Growth Pockets” IRI finds that consumers are resuming active lifestyles while maintaining at-home habits (e.g., more meals at home). While CPG demand has remained elevated in the first half of 2021, the analysts anticipate that demand patterns will shift as the economy reopens and there is more competition for the consumers’ wallets. The report highlights key 2021 trends and identifies emerging growth pockets for CPG manufacturers and retailers.

CHANGING SHAPE OF THE CPG DEMAND CURVE

- Consumers are becoming more comfortable shopping in stores, reverting to multiple channels (i.e., non-grocery, small format), while at the same time, many shoppers will stick with online options – behavior that will continue to drive omnichannel sales.

- Younger and higher-income households drive increasing, smaller trips; low-income households represent the highest growth opportunity as they continue to spend more for home consumption.

- CPG demand continues to be idiosyncratic, with highly elevated consumption of frozen foods and baking ingredients reverting but still above the norm, while consumption of sports drinks, sleep remedies and kitchen storage and plastic drinkware remains high. Depressed categories such as cosmetics recover, yet remain below pre-pandemic sales levels.

- Consumers continue to buy premium products while shelf price increases continue to take effect. Expect increasing trade-off vs. product value as prices creep up.

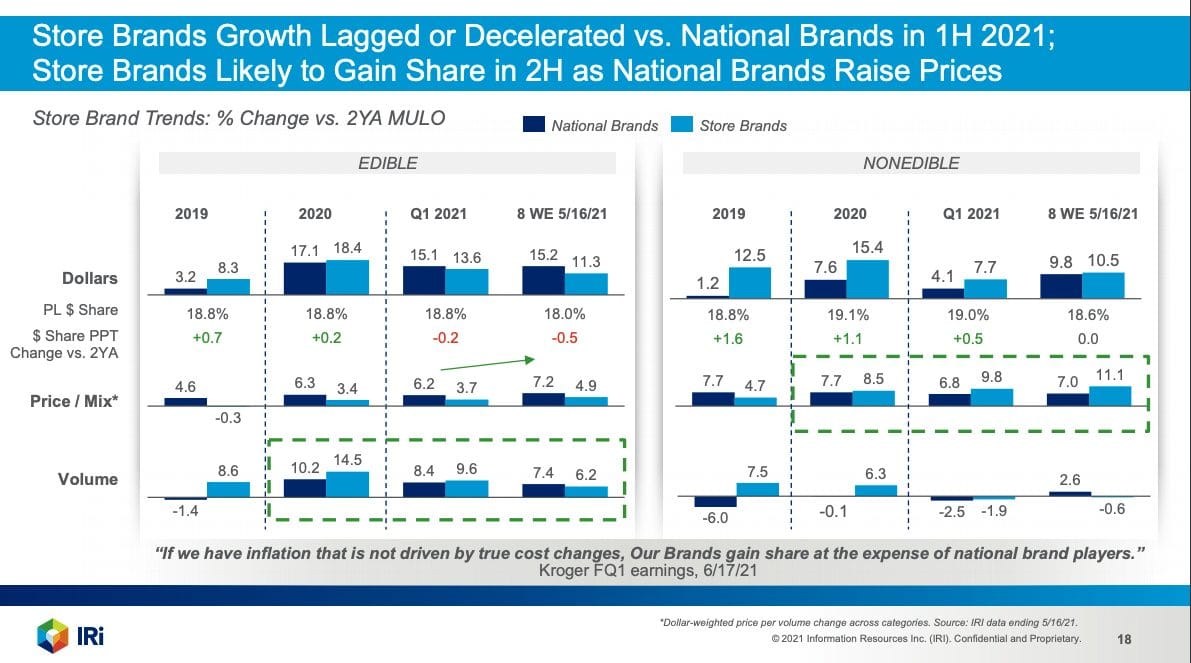

- Private brands, which lagged or decelerated vs. national brands in the 1H 2021, are likely to gain share in 2H as national brands raise prices.

- Holiday celebrations are shifting back to larger events.

- 28% of the top 100 brands gained significant penetration in 2020 and retained >50% of gains in 2021. Manufacturers and retailers will compete to win or retain penetration acquired in the last few quarters.

EMERGING OPPORTUNITIES

- Be adept at detecting shifts in consumer needs and preferences, and react with agility as demand patterns shift.

- As significant shelf price increases occur, manufacturers and retailers will have to resort to granular revenue management strategies to drive profitable growth (e.g., net price realization, truly incremental promotions, price-pack-channel range architecture).

- CPG companies cutting media budgets to offset cost inflation should optimize media ROI in real-time and focus on the right products, vehicles (e.g., digital, social) and the right segments and audiences that are most responsive to media to minimize share loss.

- Simplify the shelf set with the right placement and tailor the assortment to digital and omnichannel shoppers.

- Communicate and innovate on attributes and benefits that matter to shoppers and ensure that innovation is incremental.

- CPG retailers and manufacturers must continue to invest in online platforms to retain omnichannel shoppers and carefully curate the online vs. in-store experiences. • Focus on winning retailers, categories, brands, and channels (including on-the-go, food service) for growth

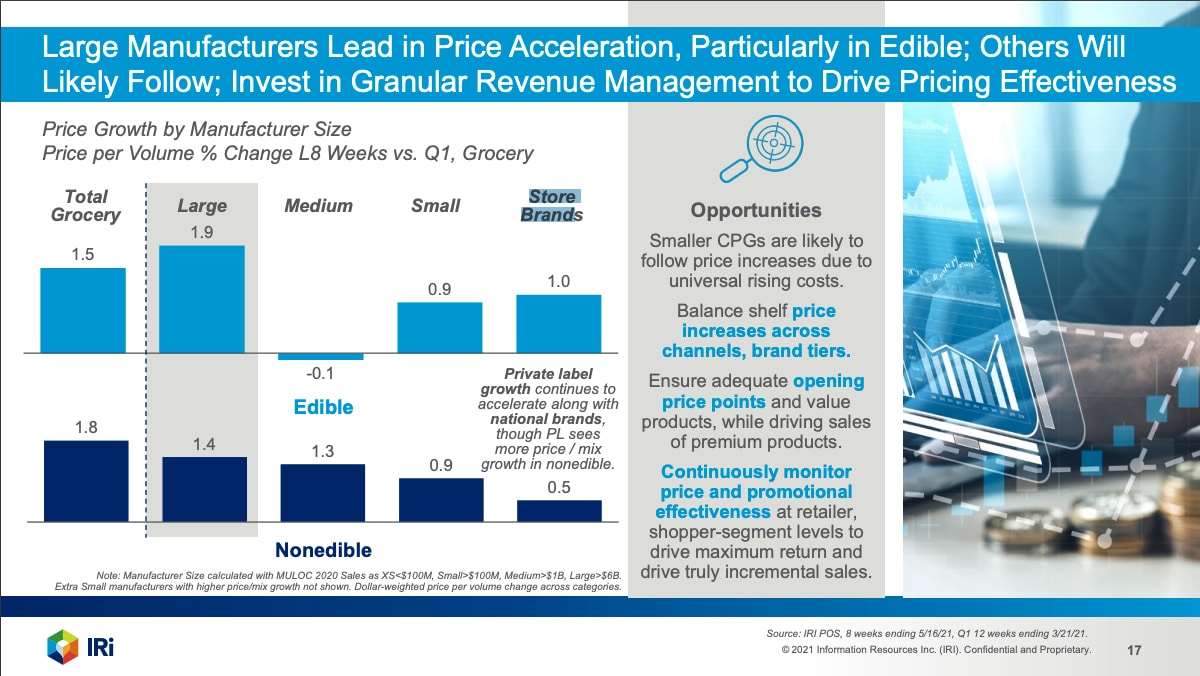

According to the report large national brands are leading in raising prices across grocery categories with private brand pricing following in food and beverages. Medium and small national brands have so far resisted the urge to increase pricing, but according to IRI, they will likely succumb to the pressure of rising costs.

Private Brand premiumization of private brands continues to trend as IRI sees an increase in SKUs in the premium price tier vs. a value tier. There has been a 15%+ increase in premium edible products pre-COVID 2020 and into the second quarter of 2021 compared with last year. Nonedible products in the premium price tier are up more than 19%.

About the Author: Bull Horn

2025 EVENTS

TICKETS, SPONSORSHIPS & EXPO BOOTHS NOW AVAILABLE